Mostbet Hindistan Rəsmi Saytı 25,000 Pulsuz Oyna Başlanğıc Və Qeydiyyat

Nyc Incontri Coach: Mock Schedules e Improv Sessions Assist Singles Think on Their Ft Whenever It Count

Instead of counting these as 200 incomplete bars, we use equivalent units to measure them. Since they are halfway done, it’s like having 100 fully completed chocolate bars. This helps the factory calculate costs more accurately for the partially finished products.

What’s the point of process costing?

FIFO (First-In, First-Out) and WA (Weighted-Average) are methods used to assign costs to units produced. FIFO assumes that the oldest costs are assigned to the units completed first. For example, for a factory is making chocolate bars, FIFO means the cost of the ingredients and labor from the beginning of the production period are used first to calculate the cost of the finished bars. This helps to track the flow of costs more accurately based on the production timeline.

Step 3 of 3

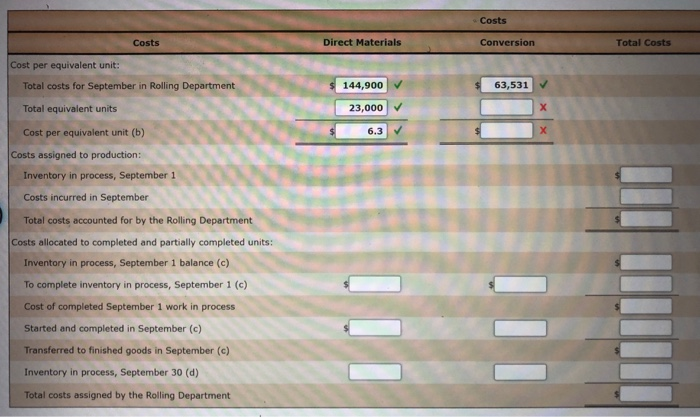

To calculate the cost per equivalent unit formula, you must divide the total production costs assigned in the process by the equivalent units of production. This will give you the cost that can be allocated to each equivalent unit produced during the period. This report shows the costs used in the preparation of a product, including the cost per unit for materials and conversion costs, and the amount of work in process and finished goods inventory. A complete production cost report for the shaping department is illustrated in Figure 8.71. Direct material is added in stages, such as the beginning, middle, or end of the process, while conversion costs are expensed evenly over the process.

2 Equivalent Units (Weighted Average)

In the previous page, we discussed the physical flow of units (step 1) and how to calculate equivalent units of production (step 2) under the weighted average method. We will continue the discussion under the weighted average method and calculate a cost per equivalent unit. Managerial and cost accountants use the equivalent units of production to allocate production costs to units during the manufacturing process. For instance, calculating the cost of goods produced is simple if there is no beginning or ending goods in process inventory.

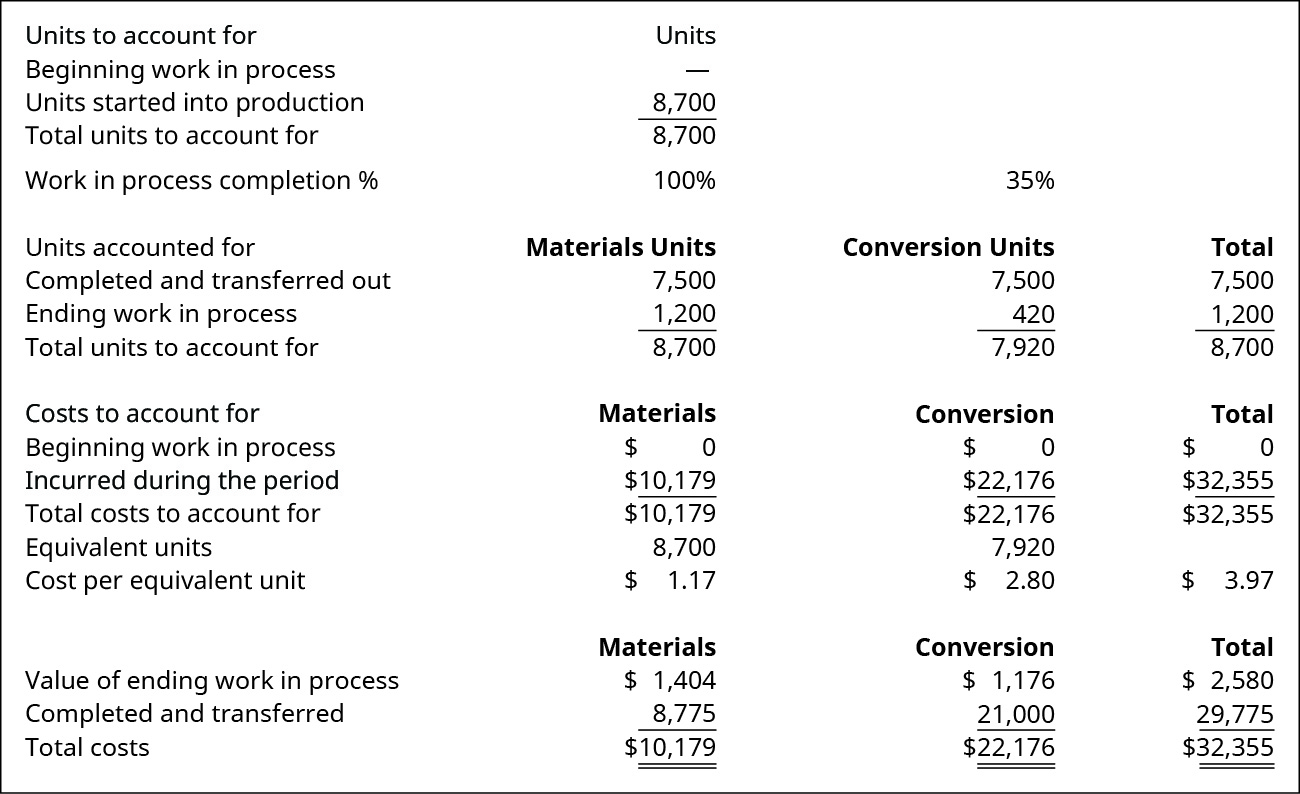

If these defects are non recurring then such units should be excluded from equivalent production. Finally, the equivalent units of production calculated via the previous three steps should be aggregated to ascertain the total output in terms of equivalent units or equivalent production. We started with 750 units that were 100% complete as to materials and 60% processed, so the beginning work-in-process EUs for direct materials is 0% of 750 and for conversion costs is 40% of 750 which is 300. To calculate cost per equivalent unit by taking the total costs (both beginning work in process and costs added this period) and divide by the total equivalent units. While process costing tracks costs for huge number of identical products, job costing tracks costs for specific, individual jobs or orders, which are often unique.

For example, forty units that are \(25\%\) complete would be ten (\(40 × 25\%\)) units that are totally complete. We have 4,000 total units for which to account, with 750 in process at the beginning of the month, and the last batch that is still in process at the end of the month will be 1,000 shells once it is done. On the last day of February, it was only 25% through the process, meaning that the EUs for ending inventory for direct materials was 1,000 units and for conversion costs was 25% of 1,000 units which is 250 EUs. For costs of units completed and transferred, we take the equivalent units for units completed x cost per equivalent unit. We do the same of ending work in process but using the equivalent units for ending work in process.

Conversion costs are those costs incurred to convert raw materials into the final product (meaning, direct labor and overhead). To illustrate more completely the operation of the FIFO process cost method, we use an example of the month of June production costs for a company’s Department B. Department B adds materials only at the beginning of processing. The May 31 inventory in Department B (June’s beginning work in process) consists of 2,000 units that are eligible child fully complete as to materials and 60% complete as to conversion. The calculation of equivalent units depends on the cost flow assumption used i.e. the calculation is different for first-in-first-out and weighted average. In the weighted average method, total equivalent units for the process for a period are calculated using the following formula. For example, a factory is making chocolate bars and they have 200 bars that are halfway done at month-end.

Therefore, there are a few more steps in creating the Production Cost Report. However, the first step is the same as with the weighted average method. The problem will provide the information related to beginning work in process inventory costs and units. Weighted average takes the units completed during the period and adds it to your ending WIP. For example, during the month of July, Rock City Percussion purchased raw material inventory of \(\$25,000\) for the shaping department. Although each department tracks the direct material it uses in its own department, all material is held in the material storeroom.

Reconciling the number of units and the costs is part of the process costing system. The reconciliation involves the total of beginning inventory and units started into production. Units completed and transferred arefinished units and will always be 100% complete for equivalent unitcalculations for direct materials, direct labor and overhead. Forunits in ending work in process, we would take the units unfinishedx a percent complete.

We want to make sure that we have assigned all the costs from beginning work in process and costs incurred or added this period to units completed and transferred and ending work in process inventory. These costs are then used to calculate the equivalent units and total production costs in a four-step process. In the current period, we transferred 500 units to process 2, and have 350 equivalent units in our WIP inventory. So our equivalent units of production for the period would be 850 units. Essentially saying, that process 1 completed 850 units to completion of process 1 in this period. The 750 shells in production at the end of January were 60% complete as to conversion costs and 100% complete as to direct materials, so in February they will need 40% more conversion but 0% more direct materials.

- For example, during the month of July, Rock City Percussion purchased raw material inventory of \(\$25,000\) for the shaping department.

- Then, we compare the total to the cost assignment in step 4 for units completed and transferred and ending work in process to get total units accounted for.

- The equivalent unit computation determines the number of units if each is manufactured in its entirety before manufacturing the next unit.

- FIFO (First-In, First-Out) and WA (Weighted-Average) are methods used to assign costs to units produced.

- Weighted average takes the units completed during the period and adds it to your ending WIP.

All of the units transferred to the next department must be 100% complete with regard to that department’s cost or they would not be transferred. So the number of units transferred is the same for material units and for conversion units. The process cost system must calculate the equivalent units of production for units completed (with respect to materials and conversion) and for ending work in process with respect to materials and conversion. All of the units transferred to the next department must be \(100\%\) complete with regard to that department’s cost or they would not be transferred. In addition to the equivalent units, it is necessary to track the units completed as well as the units remaining in ending inventory. A similar process is used to account for the costs completed and transferred.

Trackbacks and Pingbacks