6 7: Product vs. Period Costs Business LibreTexts

Men's room Incontri Expert Kezia Noble offers Honest Feedback to Singles in sunday Bootcamps & Mastery Programs

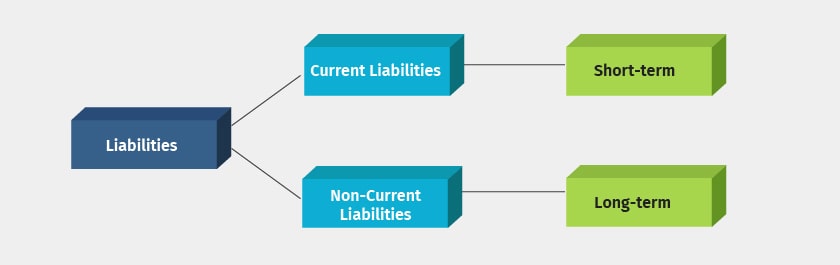

A liability is anything that’s borrowed from, owed to, or obligated to someone else. It can be real like a bill that must be paid or potential such as a possible lawsuit. A company might take out debt to expand and grow its business or an individual may take out a mortgage to purchase a home.

- The final rule modifies the proposal to specify that the agencies will take into account the liquidity, maturity, and depth of the market for the relevant types of financial instruments when determining whether to rebut the presumption of compliance.

- The entity is forced to reclassify all its held-to-maturity investments as available-for-sale (see below) and measure them at fair value until it is able, through subsequent actions, to restore faith in its intentions.

- Current liabilities can also be settled by creating a new current liability, such as a new short-term debt obligation.

- Although this option is not explicitly available for financial assets, there’s no need for it as financial assets managed on a fair value basis would fall into the FVTPL category based on the business model criterion.

- The only exemption to this are equity securities that do not have a quoted market price in an active market and for which a reliable fair value cannot be reliably measured.

Categories of financial liabilities under IFRS 9

Current liabilities are typically settled using current assets, which are assets that are used up within one year. Current assets include cash or accounts receivable, which is money owed by customers for sales. The ratio of current assets to current liabilities is important in determining a company’s ongoing ability to fixed asset turnover ratio formula calculator pay its debts as they are due. Furthermore, the presence of sales in a portfolio does not negate a business model aimed at collecting contractual cash flows. For instance, sales triggered by an increase in the credit risk of financial assets, regardless of their frequency or value, align with the model’s objective.

Current Liabilities: What They Are and How to Calculate Them

A business model whose objective is to hold assets in order to collect contractual cash flows emphasises managing assets primarily for the collection of their contractual cash flows over their life, rather than for overall portfolio returns through both holding and selling. In assessing whether a business model is oriented towards collecting these cash flows, it’s crucial to consider the historical pattern of sales – their frequency, value, timing, and the reasons behind them – in conjunction with expectations about future sales activities. Thus, an entity must evaluate past sales in light of the reasons for these sales and the conditions at that time, comparing them with the present conditions. The business model’s essence lies in its approach to generating cash flows, whether through collecting contractual flows, selling assets, or a combination of both.

Contractual cash flow characteristics (‘SPPI test’)

This publication is not a substitute for such professional advice or services, nor should it be used as a basis for any decision or action that may affect your business. Before making any decision or taking any action that may affect your business, you should consult a qualified professional advisor. AP typically carries the largest balances because they encompass day-to-day operations. AP can include services, raw materials, office supplies, or any other categories of products and services where no promissory note is issued. Most companies don’t pay for goods and services as they’re acquired, AP is equivalent to a stack of bills waiting to be paid.

Tax liability can refer to the property taxes that a homeowner owes to the municipal government or the income tax they owe to the federal government. A retailer has a sales tax liability on their books when they collect sales tax from a customer until they remit those funds to the county, city, or state. Traders should be well-versed in the different types of liabilities, the distinction between liabilities and provisions, and the reasons why monitoring liabilities is vital for their trading success. Effective management of liabilities not only ensures a trader’s financial stability but also paves the way for sustainable growth and profitability in the world of trading. Traders must have a clear picture of their current liabilities as they impact short-term cash flow and liquidity.

Secondly, there exists a perceived economic relationship between these assets and liabilities. For instance, a liability may be perceived as related to an asset if they share a risk that causes opposite changes in fair value that typically offset each other, or when the entity considers the liability as funding for the asset (IFRS 9.BCZ4.61). For practical reasons, the entity doesn’t have to enter into all the assets and liabilities creating the accounting mismatch simultaneously (IFRS 9.B4.1.31). Trading assets are mostly owned by financial firms that have business segments involved in trading or investing in securities markets.

Trading assets are listed on the balance sheet at fair value and reported as current assets. Unrealized gains and losses are included in accumulated other comprehensive income within the equity section of the balance sheet. For example, if a company purchases shares of ABC company for $2 million, and ABC’s shares drop in value by 30%, the company would adjust the value of the trading assets to $1.4 million on the balance sheet and record a net loss of $600,000 on the income statement. Liabilities are listed on a company’s balance sheet and expenses are listed on a company’s income statement. Expenses can be paid immediately with cash or the payment could be delayed which would create a liability. Any liability that’s not near-term falls under non-current liabilities that are expected to be paid in 12 months or more.

Another instance is a financial services firm closing its retail mortgage sector, ceasing new business and actively selling its mortgage loan portfolio. However, mere changes in intentions towards specific financial assets, reactions to market condition fluctuations, the temporary loss of a market, or transfers of assets between different business models within an entity do not qualify as changes in the business model (IFRS 9.B4.4.1-3). The agencies continue to consider whether the approach being adopted in the final rule may be extended to other issuers, such as funds advised by the banking entity, and intend to address and request additional comment on this issue in the future proposed rulemaking. The 2013 Rule permits certain foreign banking entities, subject to several conditions set forth in the rule, to engage in proprietary trading outside of the United States. The final rule removes the condition in the 2013 Rule that no personnel of the foreign banking entity that arrange, negotiate, or execute the purchase or sale be located in the United States. The limits used to satisfy the presumption of compliance under the final rule will be subject to supervisory review and oversight by the applicable agency on an ongoing basis.

Trackbacks and Pingbacks